Doing the Boldest Things in the Riskiest Field

Most biotech VCs back the second mouse. One firm only does first-in-category — and personally built Moderna, Editas, and Indigo Agriculture along the way.

- #biotech

- #venture-capital

- #innovation

- #flagship

Originally published November 2 2018 on 生息资讯, a WeChat publication I ran with friends from 2017 to 2021. Pen name: 平平喵喵喵 (after my cat Pingping).

Foreword

Biotech venture capital has long been considered an uphill climb: huge upfront investment, high technical risk, dense regulatory constraints, long return cycles. Most innovation and entrepreneurship in the field stays close to existing theory and technique — incremental innovation by another name.

And yet, there’s a US-based early-stage VC focused entirely on biotech that says: “If someone else is doing it, we won’t. We only do first-in-category.” This is the firm that personally built dozens of world-class biotech companies — Editas Medicine, Indigo Agriculture, Moderna Therapeutics.

It’s called Flagship Pioneering. What did this audacious — and now genre-defining — investor actually do?

1. The Uncertain Challenge — Standing in No-Man’s Land

In 1999, Dr. Noubar Afeyan stepped back from the three companies he’d helped build over the previous decade. At 37, he started looking back over those experiences, trying to systematize a method for science-driven entrepreneurship. That same year he founded NewcoGen (short for “New Company Generator”) — later renamed Flagship Venture, and now Flagship Pioneering. After 18 years of practice, Flagship has become the undisputed leader in early-stage biotech VC, and is studied as a textbook case at Harvard Business School.

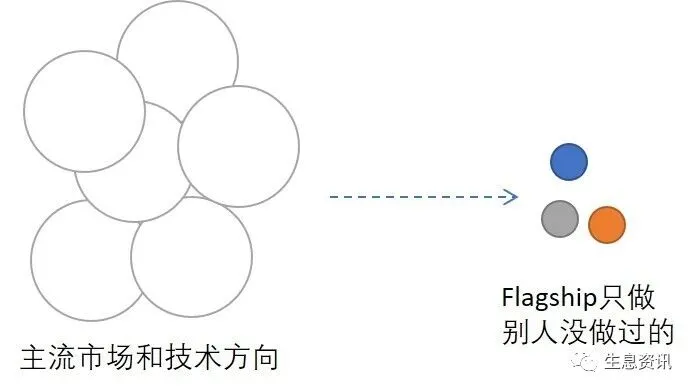

The thing that draws the most attention to Flagship is their declared stance: we only do first-in-category breakthroughs. Picture it like this:

This positioning has an obvious upside (and many less-obvious ones — you’ll see them if you look):

- Zero competition. If you pull it off, the result, the IP, the market — all yours.

The downsides are equally obvious:

- Zero foundation. No external reference points; no way to lean on platform technology for incremental innovation.

- Every link in the chain has to be figured out internally. The relevant academic and industrial communities aren’t yet mature, so collaboration, leverage, or outsourcing are rare.

- Extreme uncertainty. Risk doubles. The cycle doubles.

- Technology too far ahead. Downstream investors may not be ready.

Note the word do. Why not just invest? Because the vast majority of Flagship’s projects really are done — incubated end-to-end inside the firm.

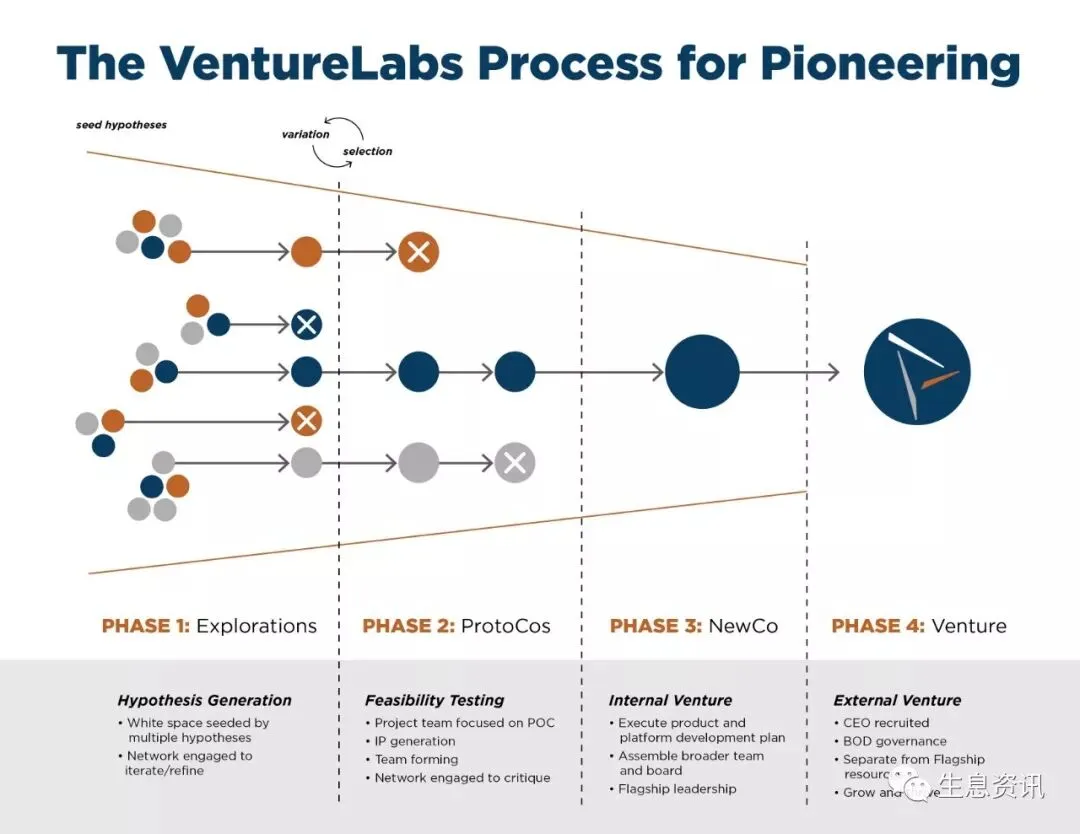

2. The Certain Process — A Systematic Method of Exploration

“To make progress in extremely uncertain new territory, we need an extremely well-defined methodology,” Afeyan has said. “The same way life itself, through tight genetic rules, gradually evolved exquisite designs adapted to all kinds of uncertain environments.”

Flagship has never been shy about publicizing its venture-creation process. Briefly, four phases:

- Exploration — form the hypothesis

- Prototype — run the killer experiment on the critical question

- Internal company — commercial buildout

- Spin-out — independent operation

It sounds similar to most innovation processes, but note one thing: in the first three phases, Flagship is personally on the team, personally writing the checks, personally participating.

Phase 1: Forming a valuable hypothesis

The core of the exploration phase is forming a valuable hypothesis. Each year Flagship recruits a fresh class of top-school biology PhDs and MBAs as trainees, lets them team up in twos and threes, and — under a partner’s lead — lets their imaginations run on “possibilities,” or hypotheses. Hundreds of these “possibilities” surface inside Flagship every year, then go out to its industry and academic network for stress-testing and critique.

At this stage, “possibilities” are protected as much as possible. Advisors are explicitly told not to evaluate technical feasibility; what they’re evaluating is if this worked, how much value would it create. They ask: “Why couldn’t we do this?” and “If this turned out to be feasible, what could we build?”

Most of the original “possibilities” don’t survive to the end. But the ones that do — the ones eventually agreed to be valuable — usually trace back to the wild ideas at the start. Roughly 3–6 months in, around a dozen “possibilities” have made it through.

Phase 2: Proof of principle, killer experiments

These ideas now enter Flagship’s own 5,500-square-meter shared lab, to be challenged by a 40-person full-time scientist team. The team’s job is simple: expose the project’s critical technical or logical flaws as ruthlessly as possible, and kill it early. Flagship calls this the Killer Experiment.

The phrase isn’t new — many companies and academic groups claim to follow the logic — but very few actually do it:

- Academia can’t — because researchers need outputs and publications.

- Industry can’t — because if the project dies, the people working on it lose their jobs.

- Investors don’t want to — because for an existing portfolio company, finding the next sucker to take it off your hands counts as an “exit,” and an exit counts as success.

Flagship makes killer experiments real through mechanism design:

- For the fund itself: the money and people at this phase are theirs. A few million dollars — die early, die cheap. There are still a dozen other candidates waiting. If a fatally flawed project sneaks into the next phase, the investor is still Flagship — and now the loss is tens of millions.

- For the scientist team: their livelihood barely depends on any single project. They get to spend full time at the frontier of the field, and if one direction doesn’t work, several others are already lined up. Flagship even uses numeric code names for projects, on purpose, to keep researchers from getting attached to a specific “possibility” and burying problems.

Phases 3 and 4: Team building and independence

A “possibility” that survives the killer experiment enters phase 3. Flagship begins assembling a real company around it. A partner steps in as transition CEO and starts hiring outside, building a 20–30 person team. Flagship’s fund now formally becomes the lead Series-A investor, putting in tens of millions of dollars and — as the founding institution — controlling most of the equity. Typically a Flagship project only becomes externally visible at this third phase. By then it’s already passed its key proof-of-concept, and is in orderly R&D and commercial buildout.

Once the company is structurally stable and running smoothly, Flagship finally feels confident cutting it loose from the shared resources — making it a fully independent company, entering phase 4, opening to outside investment. Top-tier outside investors like Polaris Partners and Third Rock Ventures pile in, eager to deploy hundreds of millions. Even so, having been hands-on through phases 1 to 3, Flagship still holds a percentage of equity that ordinary VCs can only dream of.

3. The Triumph of “Possibilities”

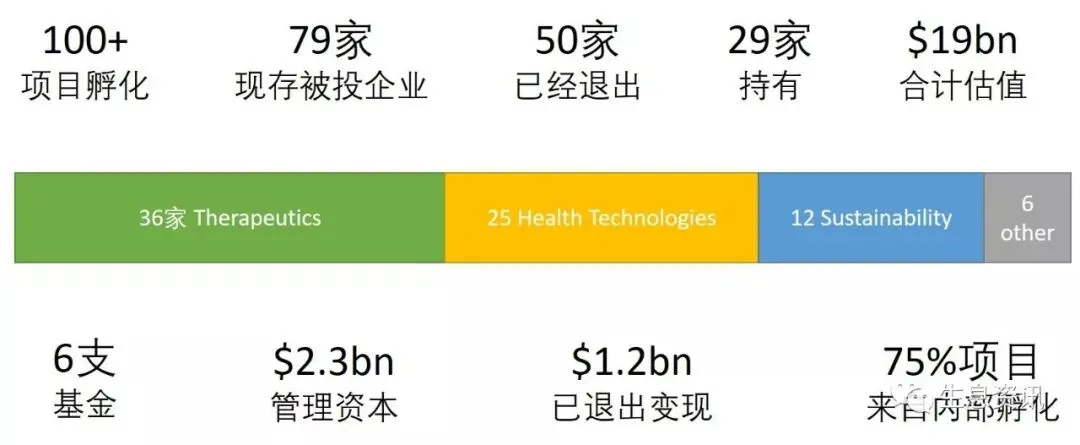

Enough framing — let’s look at Flagship’s record so far this year.

From 2000 to today, 18 years have proven the model’s quality. Per a 2017 mid-year report, both Fund IV and Fund V rank in the top three globally for biotech VC returns of their vintage.

A few of the names Flagship has incubated:

![]()

Indigo Agriculture — the world’s leading agricultural microbiome company.

![]()

Editas Medicine — developing new therapies based on CRISPR-Cas9 gene editing.

![]()

The most remarkable of them all is Moderna Therapeutics, the world’s first and still leading mRNA-drug developer. Flagship led every single VC round of the company itself, and remains its largest shareholder. Moderna has since received over $1 billion in strategic investment from AstraZeneca, Alexion, Merck, and others — a complete demonstration of Flagship’s incubation methodology.

There are many other star companies I won’t list one by one.

Flagship’s 2017 numbers look like this:

- 2 IPOs: Denali Therapeutics (NASDAQ: DNLI) and Quanterix (NASDAQ: QTRX)

- 40 brand-new therapies in clinical trials

- 1 FDA approval: Agios Pharma’s IDHIFA

- $835 million in external equity financing across portfolio companies

- 6 companies successfully spun out of incubation

- 2 companies went from stealth to public

- $618 million raised for Fund VI

4. Closing — On “Risk,” “Creativity,” and “Drive”

If we kept going, this could easily become two more articles — let’s stop here for now. To close, a few questions worth chewing on:

- The full-time scientist team and killer-experiment loop sit at the core of Flagship’s risk management. Can the model be transplanted outside biotech? What conditions would have to be met?

- Some “possibilities” carry too much risk — too much for entrepreneurs to bear, too speculative for big companies to fund. What mechanism does Flagship use that lets these possibilities get explored at all?

- The full-time people inside Flagship’s incubator are top-school or top-firm talent. What design lets them collect a steady salary (and very little equity), keep entrepreneur-grade exploration energy, and not jump ship?

References:

- Luo, Hong, Gary P. Pisano, and Huafeng Yu. “Institutionalized Entrepreneurship: Flagship Pioneering.” Harvard Business School Case 718-484, January 2018. (Revised April 2018.)

- http://flagshippioneering.com/process/

- https://www.forbes.com/sites/luketimmerman/2015/03/26/flagship-ventures-snags-537m-to-get-in-at-the-ground-floor-in-biotech/

- http://flagshippioneering.com/news/flagship-pioneering-announces-capital-raise-618mm/

Particular thanks to Professor Hong Luo of Harvard, whose case-study presentation at MIT inspired much of the analysis here.